Returns Trend Promising")

If you want to find stocks with long-term growth potential, what underlying trends should you look for? First, you want to identify stocks that are growing. return Return on Invested Capital (ROCE) and in parallel, base 100% of invested capital. When you see this, it usually means it's a company with a good business model and lots of profitable reinvestment opportunities. Speaking of which, we've noticed some big changes. I-Tech Let's take a look at (STO:ITECH)'s return on capital.

What is Return on Invested Capital (ROCE)?

For those unfamiliar, ROCE is a metric that assesses how much pre-tax profit (as a percentage) a company earns on the capital invested in its business: Here's the formula for calculating this at I-Tech:

Return on Invested Capital = Earnings Before Interest and Taxes (EBIT) ÷ (Total Assets – Current Liabilities)

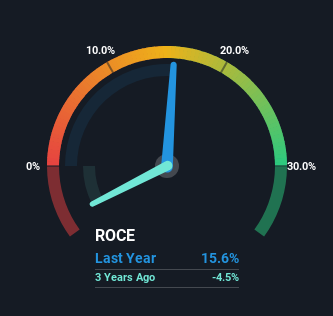

0.16 = kr23m ÷ (kr163m – kr18m) (Based on the trailing 12 months ending March 2024).

therefore, I-Tech has an ROCE of 16%. That's a standard return in itself, but it's still much better than the 11% generated by the chemical industry.

Check out our latest analysis for I-Tech

Above we can see how I-Tech's current ROCE compares to its prior returns on capital, but the history can only tell us so much, and if you'd like to see what analysts are predicting going forward you can take a look at this free analyst report on I-Tech.

What can we learn from ROCE trends?

We're pleased to see I-Tech is profiting from its investments and generating pre-tax profits. Shareholders will no doubt be pleased with this, as a business that was unprofitable five years ago is now generating a 16% return on capital. And, as expected, like most companies looking to turn a profit, I-Tech has 32% more capital deployed than it did five years ago. This suggests the company has plenty of opportunities for reinvestment that could generate higher returns.

Our take on I-Tech's ROCE

In summary, it's great to see I-Tech maintaining profitability and continuing to reinvest in its business. Total stock returns have been fairly flat over the past five years, so there may be an opportunity at a good valuation. Therefore, it seems reasonable to investigate this company further to determine whether these trends will continue.

However, I-Tech has some risks and we 2 warning signs for I-Tech Something you might be interested in.

If you want to find solid companies with profitable returns, check these out free A list of companies with strong balance sheets and good return on equity.

Valuation is complicated, but we can help make it simple.

investigate ITEC By checking our comprehensive analysis, you can see whether it may be overvalued or undervalued. Fair value estimates, risks and warnings, dividends, insider trading, financial strength.

View your free analysis

Have feedback about this article? Concerns about the content? contact Please contact us directly. Or email editorial-team (at) simplywallst.com.

This article by Simply Wall St is of general nature. We use only unbiased methodologies to provide commentary based on historical data and analyst forecasts, and our articles are not intended as financial advice. It is not a recommendation to buy or sell stocks, and does not take into account your objectives, or your financial situation. We seek to provide long-term focused analysis driven by fundamental data. Note that our analysis may not take into account the latest price sensitive company announcements or qualitative material. Simply Wall St has no position in any of the stocks mentioned.